Canadian Productivity “OR” Economic Resilience?

How to align economic forces to increase labor productivity and economic resilience.

Kirk

2/13/20254 min read

Canadian Productivity “OR” Economic Resilience?

How About “AND”

There is a lot of discussion in Canada right now about the need to increase our economy's productivity and resiliency. Our labor productivity has not kept pace with the United States over the past decade, and with the threat of trade tariffs, our economy is particularly vulnerable. Productivity and resilience are two separate attributes of an economy. Many economic forces/laws affect how productivity and resilience relate. These economic forces can cause productivity and resilience to be negatively correlated in the short term or positively correlated at other times. As leaders and managers, it is important to understand the tensions these economic attributes have on each other to optimize businesses and industries to increase both productivity and resilience. Below, we will review three economic forces and their impact on productivity and resilience. These forces include diversification vs specialization, economies of scale, and capital investment.

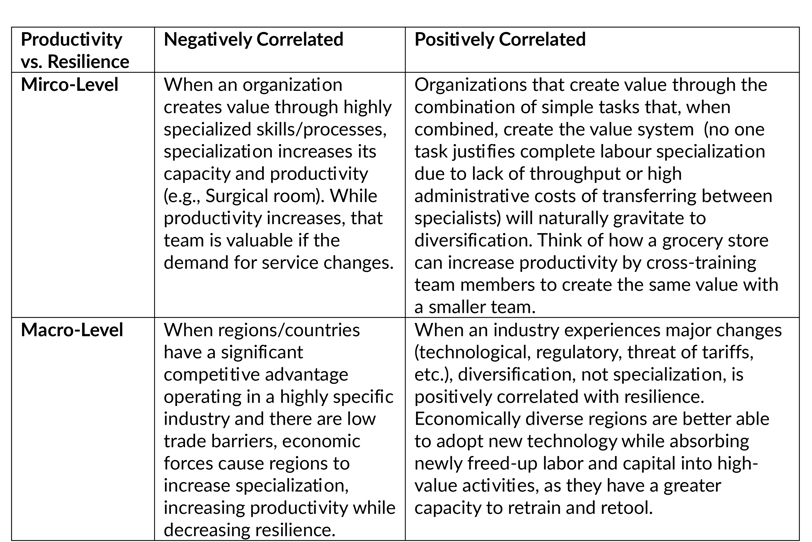

Diversification vs. Specialization (generally negatively correlated, but an argument can be made for positive correlation if properly managed): Labour specialization can occur at both micro and macro levels (see table below). How can we determine the best mix of specialization in our organizations?

Economies of Scale (negatively correlated): Economies of Scale often lead to increased production/labor hours. When building systems to support economies of scale, organizations give up flexibility for higher throughput. This is very important in commodity industries, as economies of scale enable profit margins in “price taker” industries. However, economies of scale often lead to a trade-off between the reliability and productivity of an organization in the short term. How can organizations use economies of scale to increase productivity and, in the long term, increase resilience? How do we balance the role of monopolies for the ability to fund innovation with the need for competitive markets to refine innovation?

Capital Investment (negatively correlated): Capital investment in productive assets increases productivity. Capital can come from debt or equity and can be transformed into assets with varying degrees of liquidity. When an organization transforms liquid capital (ex., Cash) into illiquid capital (ex., Manufacturing equipment), it loses flexibility for productivity. When debt financing is used, these effects can be multiplied as debt coverage costs can eat into an organization's runway for funding changes in its value-creation process, making it less resilient. How can organizations fund capital investments while minimizing the erosion of resilience?

These are just a few of the many economic forces that affect productivity and resilience. The better we understand the laws of economics, the better we apply them to propel our organizations forward. In general, increased productivity leads to increased margins that can be used to either further increase productivity, fund new opportunities to increase resilience in the long term, or fund unproductive consumption. The challenge for leaders is how to distribute margins that positively impact our businesses and economy.

While some economic forces, at the surface, cause a negative correlation between productivity and resilience, leaders can create environments where these forces are more aligned; thus, we can increase both productivity and resilience. Jim Collins discusses the Genius of the AND in his book "Built to Last." As leaders, we can elevate our problem-solving by placing constraints on the solutions we seek. For example, when Toyota was trying to compete with American car manufacturers that had greater economies of scale, Toyota focused on increasing productivity and resiliency by implementing SMED (single-minute digit exchange of die). This allowed Toyota to have smaller batch sizes and create more differentiated products with less capital investment.

When leaders require solutions to increase resilience and productivity, innovative solutions are required. These innovative solutions are necessary to make progress on closing our productivity gap while becoming less dependent on trade with the United States. The closer we are to a problem, the more efficiently and effectively we can apply resources to solve it. As a result, tangible gains in economic prosperity should start at the individual and organizational levels and then filter up to the political level.

We all have a part to play in revitalizing our economy. It takes effort and will require us to have a deeper understanding of our value creation systems. Fortunately, investing in deepening our understanding of our value creation systems continues to pay dividends in stable and turbulent economic times. These dividends come in the form of increased productivity and value, which result in increased margins. These margins can be reinvested to spark a productivity revolution and lead to a more resilient economy for all Canadians.

Productivity vs. Resilience Negatively Correlated Positively Correlated

Mirco-Level When an organization creates value through highly specialized skills/processes, specialization increases its capacity and productivity (e.g., Surgical room). While productivity increases, that team is valuable if the demand for service changes. Organizations that create value through the combination of simple tasks that, when combined, create the value system (no one task justifies complete labour specialization due to lack of throughput or high administrative costs of transferring between specialists) will naturally gravitate to diversification. Think of how a grocery store can increase productivity by cross-training team members to create the same value with a smaller team.

Macro-Level When regions/countries have a significant competitive advantage operating in a highly specific industry and there are low trade barriers, economic forces cause regions to increase specialization, increasing productivity while decreasing resilience. When an industry experiences major changes (technological, regulatory, threat of tariffs, etc.), diversification, not specialization, is positively correlated with resilience. Economically diverse regions are better able to adopt new technology while absorbing newly freed-up labor and capital into high-value activities, as they have a greater capacity to retrain and retool.

Learn

Catalyzing success for operators of small and medium businesses.

community@operatorscatalyst.com

780-217-8301

© 2025. All rights reserved.